The Implicit Debt of Social Security Systems In the EU: Challenges to Bulgaria

Dragomir Belchev*, February 27, 2012

In February 2012 the European Commission has published a White Paper on adequate and sustainable pensions. The document aims to re-sharpen European public opinion's attention on the problems associated with ageing. This process will only intensify in coming years, as it will put on trial the social security systems structure that cover not only pensions but also health care and long term care for the elderly. In times of budget constraints the main problem is not just how to spend the money on social programmes, but how the public liabilities accumulated so far to be allocated between current and future generations. Moreover, what price the future generations would have to pay if we postpone the reduction of public debt.

In February 2012 the European Commission has published a White Paper on adequate and sustainable pensions. The document aims to re-sharpen European public opinion's attention on the problems associated with ageing. This process will only intensify in coming years, as it will put on trial the social security systems structure that cover not only pensions but also health care and long term care for the elderly. In times of budget constraints the main problem is not just how to spend the money on social programmes, but how the public liabilities accumulated so far to be allocated between current and future generations. Moreover, what price the future generations would have to pay if we postpone the reduction of public debt.

When we talk about public debt we must distinguish between the two categories

"explicit" and "implicit" debt.

The explicit debt is formed by the sum of all surpluses and deficits over the years and is a major criterion for the limits of the EU Stability and Growth Pact – deficit up to 3% of GDP and public debt up to 60% of GDP. On the other hand, this indicator does not reveal the whole truth about the fiscal burden that threatens the future. After adding the so called "implicit debt" thereto, the value will greatly exceed the specified "ceiling" of 60% of GDP.

Actually, the implicit debt is the state's promise to provide both citizens today, and those who will be born and live in the future, different benefits - such as pensions, health and long-term care. Of course, all current and future costs must be covered by the current and future tax revenues and social insurance contributions. Technically, this is the net tax that is paid individually by every citizen throughout his life (the difference between all transfers from the state in the form of pensions and other social benefits and all transfers to the state as taxes and social insurance contributions).

What, if current and future nation's spending on health, pensions and care for elderly is not covered by respective revenues of the health care, pension and long term care insurance? In that case there will be a deficit of the social security system, with the gap between revenue and expenditure being the so called sustainability gap. Adding up all gaps on an infinite basis yields the amount of implicit public debt. As it is calculated on an infinite basis, the implicit debt will overlap between generations. So we must carefully allocate its weight between them, moreover that the postponement of repayment over time will lead to higher cost and burden on future generations.

It is a matter of time the implicit debt of the EU countries to become explicit

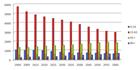

Ageing and irreversible demographic processes will contribute this to happen when the current contributions to social systems are no longer sufficient and they will fall into chronic deficit. Falling fertility and increased life expectancy in recent decades will lead to a new age structure of population. The dependency ratio of older people in the enlarged EU is expected to double to 50 in the coming decades. The total dependency ratio of the whole system will increase from 120 now to 150 in 2050: in the first case, 100 working people will have to support 50 people aged 65 and up, and in the second - 100 people will have to support 150 inactive (very young, old or unemployed). In Bulgaria this process was significantly accelerated by poor economic conditions. On the one hand many people, mainly of working age, have left the country and on the other hand - fertility has decreased dramatically. As a result the population has become the fastest shrinking in Europe (see the chart right).

this process was significantly accelerated by poor economic conditions. On the one hand many people, mainly of working age, have left the country and on the other hand - fertility has decreased dramatically. As a result the population has become the fastest shrinking in Europe (see the chart right).

Based on the indicator of the so called required adjustment in the budgets, introduced by the European Commission in 2009, (costs for current and future generations that do not meet the revenue collected within the social security system for those generations) we can calculate what are the hidden liabilities of the countries that they must overcome. The hidden public liabilities are in the table to the left as a percentage of GDP and converted into present value.

Based on the indicator of the so called required adjustment in the budgets, introduced by the European Commission in 2009, (costs for current and future generations that do not meet the revenue collected within the social security system for those generations) we can calculate what are the hidden liabilities of the countries that they must overcome. The hidden public liabilities are in the table to the left as a percentage of GDP and converted into present value.

The calculations shown in the table should be considered in several ways. Firstly, it is clear that the liabilities significantly exceed the criteria set out in the Stability and Growth Pact. In addition, these are only the implicit liabilities as the explicit public debt is already reported. Secondly, the question arises of how individual countries will deal with the distribution of the burden between current and future generations.

What policies would reduce the hidden debt?

Budget consolidation and increasing tax burden are principle solutions to reduce the hidden debt. This will mean that any postponement of the measures would transfer the burden of dealing with the problem on future generations and would benefit current ones. Given the size of the hidden debt, one separate measure would have no effect - an intelligent mix of policies is needed. The only measures to be successful are those that could correct the dependency ratios:

- Increasing retiring age and its synchronisation with life expectancy - this measure is surely the most direct one and is assessed as the most important for the reduction of hidden debt;

- Promotion of employment - particularly of people in pre-retirement or even retirement age who should have incentives to continue working;

- Encouraging immigration from other parts of the world – of secondary weight, but also an important measure. It would have a positive effect because immigrants are usually people of working age, contributing to the revenue part of the budget and in general they are more innovative and entrepreneurial. This, of course, comes with a certain social cost, and also the immigration policy is part of the common EU policies therefore a European decision on the subject is needed;

- There are also other options, such as reforms of the pension system; adjustment of health care expenditure to the ability of the insured to contribute to the health care system; recruiting more volunteers in the long term care system to keep costs under control etc.

What are the prospects of the pension system in Bulgaria?

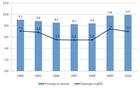

The pension system in Bulgaria also faces many challenges being part of social security system. These challenges are related to the reduction of hidden liabilities and to achieving sustainability of the system and adequate retirement benefits. Among the main problems is chronic deficit, which is topped by the state budget.** In 2010 the pension expenditure were 9.9% of GDP, their highest level in recent years.

At the same time, less labour income means less income in the form of social  insurance contributions. The main reason behind it is the replacement of the type of financing of the National Social Security Institute (NSSI) through the reduction of contributions over the years and their replacement with taxes. This has also put into question the indexation of pensions, which have been frozen during the years of uncertainty and budgetary constraints. In the context of the objective of achieving sustainability in the medium and long term (including in terms of hidden liabilities) there are several possibilities to influence the system.

insurance contributions. The main reason behind it is the replacement of the type of financing of the National Social Security Institute (NSSI) through the reduction of contributions over the years and their replacement with taxes. This has also put into question the indexation of pensions, which have been frozen during the years of uncertainty and budgetary constraints. In the context of the objective of achieving sustainability in the medium and long term (including in terms of hidden liabilities) there are several possibilities to influence the system.

1. Increasing the legal retirement age

The latest reforms were presented here quite recently, as from the beginning of 2012 the retirement age is gradually increasing by 4 months - from 60 to 63 for women, and from 63 to 65 for men. Overall, it is a good step but it is important to note that the age of people with newly granted pensions in 2010 (despite the rise in recent years) is 57 (the lowest one, compared with OECD countries), which is significantly lower than the official retirement age. Therefore, increasing retirement age itself is not sufficient to increase the revenues in the National Social Security Institute. But even if it is enough, it is likely to achieve again privileging of certain groups, classes and professions. The important lesson here is to reduce exemptions for early retirement as a reassessment is made of the different professions and positions. For better fairness and as an incentive to pay social insurance contributions, it is also required to evaluate methods of calculating pensions, by connecting more closely the individual contribution to the system.

2. Equalising retirement age between men and women

When talking about retirement, we should inevitably examine also the recommendations of the Commission to equalise the retirement age between men and women. In general, women retire earlier and receive pension benefits longer, due to higher life expectancy. On the other hand, they are more vulnerable to prolonged interruptions in their working lives, which in combination with the previous facts leads in most cases to lower pensions. Prolonging women careers would increase the amount of payments for them. It will be particularly tangible for those who are also insured in the second pillar of the pension system.

When talking about retirement, we should inevitably examine also the recommendations of the Commission to equalise the retirement age between men and women. In general, women retire earlier and receive pension benefits longer, due to higher life expectancy. On the other hand, they are more vulnerable to prolonged interruptions in their working lives, which in combination with the previous facts leads in most cases to lower pensions. Prolonging women careers would increase the amount of payments for them. It will be particularly tangible for those who are also insured in the second pillar of the pension system.

3. Promotion of private pension insurance

Besides reforming the state share of the pension system, incentives in its second and third pillar are necessary. Promoting competition between the various funds is extremely important. It can be done by removing some and reducing other levies of private pension funds and introducing a multi fund system. On the other hand, securing higher yields from the funds is linked with many other forthcoming changes, like a change in minimum yield accounting. Different incentives for voluntary pension savings will surely contribute to sustainable pension payments.

In conclusion, we can say that increasing the time people spend on the labour market should not be considered merely as an economic problem but also as a social one. In society there are many individual needs, so the system must be flexible enough to meet them. The grounds should be laid in such a way that increasing working life of people is achievable. For example, in addition to providing training and maintenance of qualifications, opportunities for flexible working hours and other possibilities should be also discussed to facilitate people in their jobs.

Despite the pessimistic trends associated with population decline, ageing and the problems of social security systems financing, this could be the beginning of a new development. The society is changing and we, as part of it, must find new solutions and opportunities. As a consequence of ageing, our value system must change and in parallel, we must develop ourselves as a society.

*The author is an expert at the Economic Policy Institute (EPI). The article represents some of the findings published in the 2011 EPI study "Implicit Debt in Public Social Security System. The case of Germany, Bulgaria, Hungary and Poland"

** Emphasis in bold are euinside`s.

| © EU

| © EU | © European Union

| © European Union | © euinside

| © euinside | © The Council of the European Union

| © The Council of the European Union | © SofiaUtre/Bonchuk Andonov

| © SofiaUtre/Bonchuk Andonov | © EU

| © EU