Rough Waters in EU

Adelina Marini, November 3, 2014

Two years have passed since the leaders of the member states tasked the four presidents (of the Commission, the Eurogroup, ECB and the European Council) to present a vision about the deepening of the integration in the euro area and since their product was approved by the heads of state or government in the end of 2012. The aim of the exercise was to find a durable solution to the eurozone's problems for which there was consensus that they were purely architectural. Jose Manuel Barroso, Mario Draghi, Jean-Claude Juncker and Herman Van Rompuy presented a road map consisting of three stages for gradual enhancing of the coordination within the euro area and practically its separation from the non-euro member states of the EU. The implementation of the first and second phases have barely been completed and the leaders of the 28 tasked them to work on a new vision. This time, however, the draft will be called the Three Presidents' report (without the Eurogroup).

Two years have passed since the leaders of the member states tasked the four presidents (of the Commission, the Eurogroup, ECB and the European Council) to present a vision about the deepening of the integration in the euro area and since their product was approved by the heads of state or government in the end of 2012. The aim of the exercise was to find a durable solution to the eurozone's problems for which there was consensus that they were purely architectural. Jose Manuel Barroso, Mario Draghi, Jean-Claude Juncker and Herman Van Rompuy presented a road map consisting of three stages for gradual enhancing of the coordination within the euro area and practically its separation from the non-euro member states of the EU. The implementation of the first and second phases have barely been completed and the leaders of the 28 tasked them to work on a new vision. This time, however, the draft will be called the Three Presidents' report (without the Eurogroup).

A desperate lack of political will

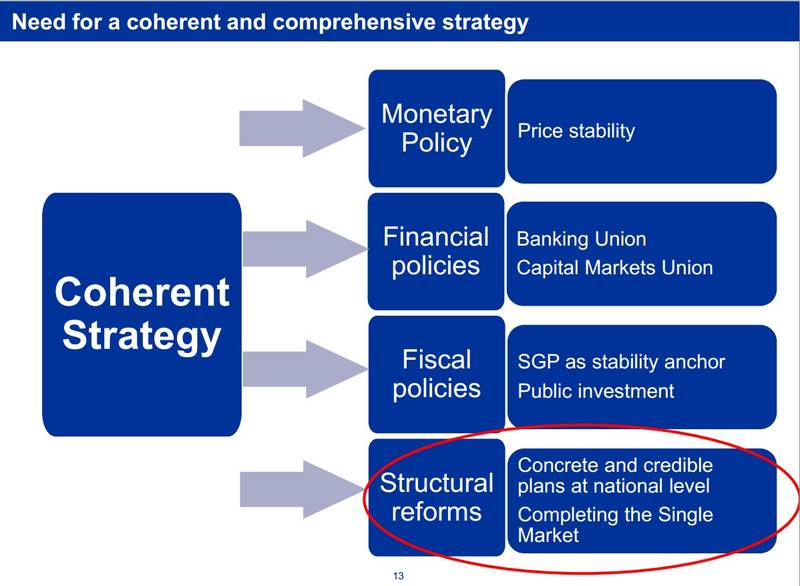

In the two-year-old report of the four presidents, it is foreseen to enhance the EU's economic governance and the eurozone's in particular and the establishment of a banking union, all of which are a fact. The third phase was the most ambitious one and included creating a common budget of the euro area and an even greater enhancement of the economic coordination among the member states. This is precisely the phase that could suffer a substantial change or it could be confirmed in the report of the three presidents. Jose Manuel Barroso, whose term ended on Friday, outran the formal presentation of the four presidents' report presenting a much more ambitious and his own vision about the development of the euro area, which foresees also treaty changes to allow the creation of a common euro area budget, the gradual issuance of eurobonds and to create a euro area ministry of finance.

The clearest results so far are from the first phase of the four presidents - the enhanced economic governance of the EU. Much longer before the report was published, the European Semester had been already functioning. It oversees the macroeconomic development of the member states and issues country-specific recommendations to remove the imbalances, whereas within the deadline set in the report the mechanism for closer coordination in the euro area has also been approved, consisting mainly of an analysis at European level of the budgetary plans of the member states that share a common currency. This exercise was done for the first time last year when the so called "two-pack" (a package of two legislative proposals) entered into force. Right before the exercise was about to be launched for a second year in a row, the tension in the EU grew dramatically mainly because of France, but fuelled by Italy, too.

The reason is, as euinside wrote, that France, although having received an extension to correct its budget deficit, proved incapable to implement the reforms recommended by the Commission. This led to speculations whether France would end up as the first member state to be punished for not sticking to its commitments under the updated Stability and Growth Pact. The Commission's behaviour toward France would have been and still is a huge test as to what extent the EU creates rules only to calm the financial markets and refuses to apply. The problem deepens additionally by the fact that the economic recovery of the euro area is not at all what everyone expected. And that is quite natural given that the recommended structural reforms are not being carried out.

France is viewed in this context in a package with Italy, but there is a substantial difference between the two. Matteo Renzi's government is trying to do, indeed, radical reforms that are met with significant resistance in the Italian parliament, but his determination to bring them to the end is visible. Moreover, he has a strategic advantage - he is very young and has still not completed his first year of governance. He is using his huge popularity and record high electoral achievements to change Italy remarkably. This is noted and appreciated in the EU, but there still is not enough confidence that he will succeed in bringing the reforms to the desired stage.

That is why, it was expected with great interest what message would the Commission convey on 29 October when it had to unveil the preliminary analysis of the draft budgets of the euro area member states they submitted on 15 October. Regretfully, the process coincided with the expiration of the mandate of Barroso's second Commission which has led to a postponement of the really important decision with two weeks. Economic affairs Commissioner Jyrki Katainen said that at that stage it was not necessary to return the budgets because "I cannot immediately identify cases of 'particularly serious non-compliance'". He underscored, however, that this did not mean that all budget plans were entirely in line with the Stability and Growth Pact.

The Commission will present a more elaborate analysis when the new European semester is officially launched and when the autumn economic forecast will be taken into account. The analysis will include an assessment of the member states' measures and the risks for the implementation of the budgets. Mr Katainen hinted that the Commission might undertake measures under the excessive deficit procedure against some member states. Probably he had in mind France. A day before the presentation of the preliminary analysis (29 October), French Prime Minister Manuel Valls was effortless in trying to persuade both the French and the European public that he is determined to implement reforms. He launched a major reformist agenda which included more or less everything France was expected to do not only this year but since the inception of the European semester.

The Commission will present a more elaborate analysis when the new European semester is officially launched and when the autumn economic forecast will be taken into account. The analysis will include an assessment of the member states' measures and the risks for the implementation of the budgets. Mr Katainen hinted that the Commission might undertake measures under the excessive deficit procedure against some member states. Probably he had in mind France. A day before the presentation of the preliminary analysis (29 October), French Prime Minister Manuel Valls was effortless in trying to persuade both the French and the European public that he is determined to implement reforms. He launched a major reformist agenda which included more or less everything France was expected to do not only this year but since the inception of the European semester.

And although what Mr Katainen presented was only a cursory analysis of the member states' measures, he admitted that there were serious consultations, especially with some member states, among which France and Italy. As a result of these talks, there were last minute corrections of the draft budgets. Such was the case of France, which initially proposed a structural effort of 0.2% (the effect of structural reforms on the budget), but later it increased it to 0.5% which Jyrki Katainen called "significant improvement". He said that he really wanted to support France in its efforts to implement structural reforms because weak growth is the result precisely of structural weaknesses. Italy, too, is doing significant changes, but the question is whether they will be implemented.

According to him, how will the taxpayers' money be spent is an entirely political decision. What is needed is political will. Jyrki Katainen quoted himself as example that, when prime minster of Finland, he had to make unpopular decisions but in the end they led to success. The decision whether France and Italy will receive an extension will be taken by the new commissioner for economic and financial affairs, Pierre Moscovici, and European Commission Vice President Valdis Dombrovskis. The awaiting of the change in the European institutions led to disappointing messages at the October European Council on 23-24 October, which are a result of serious disagreements among the member states on key economic issues.

In the conclusions from the two-day summit, the economic issues got only three points, the strongest message of which is that the structural reforms and the public finances are the key to opening investments and that against the common agreement that the macroeconomic situation is disappointing - very low gross domestic product growth, persistently huge unemployment and very low inflation, which is defined by the International Monetary Fund and the OECD as the biggest risk to the future of the European economy. Mr Barroso, the outgoing European Commission chief, said after the meeting that there are huge uncertainties lying ahead. And the problem is not only in Europe. There is a slow down of the growth of the emerging economies as well, the geopolitical situation, too, has a great impact, but the most important thing is to stop looking for ways to circumvent the EU's rules.

The agreed economic and fiscal rules should not be put into question. It is necessary to implement the country-specific recommendations. Mr Barroso said that no one demanded a change of the fiscal rules, but still there is a lot to do to implement the recommendations. The surplus countries should do more to boost domestic demand. Those that do not have sufficient fiscal space should do structural reforms mostly of the labour market, the public administration, the tax systems, the education system, but also reforms with European dimension like the completion of the internal market of energy and the digital market. Enda Kenny, the premier of Ireland, said that the situation in many countries remained fragile and quoted one of the speakers at the summit that in the euro area there are 19 different insolvency legislations.

This reduces the competitiveness of the European economies because it makes the business environment unfriendly. The rules are for everyone and should be abode, Mr Kenny added pointing out that Ireland was mentioned several times as an example that, although painful, reforms do pay back. European Central Bank's chief Mario Draghi addressed the leaders with a powerful message. This is not the first time in the past months that he urges for more attention on structural reforms at national level, warning that the ECB measures will not have a positive effect forever. He called for additional measures to share sovereignty in the economic governance but his presentation does not make it clear what exactly does he have in mind. In previous public statements he often stated his support for the four presidents' report.

This reduces the competitiveness of the European economies because it makes the business environment unfriendly. The rules are for everyone and should be abode, Mr Kenny added pointing out that Ireland was mentioned several times as an example that, although painful, reforms do pay back. European Central Bank's chief Mario Draghi addressed the leaders with a powerful message. This is not the first time in the past months that he urges for more attention on structural reforms at national level, warning that the ECB measures will not have a positive effect forever. He called for additional measures to share sovereignty in the economic governance but his presentation does not make it clear what exactly does he have in mind. In previous public statements he often stated his support for the four presidents' report.

Lithuania's President Dalia Grybauskaite, whose country will become the 19 euro area member state from 1 January, said that the discussion at the summit was "poisoned". She was absolutely resolute that the discussion about investments and political responsibility cannot be divided one from another. She recalled several times during the two-day summit that in 2005 the situation was the same with two states - France and Germany. Under pressure from these two countries, said Ms Grybauskaite, the rules of the Stability and Growth Pact were loosened. Three years later, the crisis came and some countries are still unable to recover. The Lithuanian president said that the Baltic nations are an example that without austerity measures the crisis cannot be resolved. Currently, we are growing by more than 3% and our perspective is for stable growth, she added.

Estonia's Prime Minister Taavi Roivas also said that the measures for fiscal consolidation go hand in hand with investments. Estonia is a good example because it is one of the countries that keep their budgets in balance, but also one of the countries with the highest investment rates in EU. Eurogroup chief Jeroen Dijsselbloem also excluded the possibility of changes and advised, instead, attention to be focused on what can be done. He praised Rome and Paris for their stated ambitious reforms. According to him, these reforms will modernise their society, the governments and their economies. Some of these reforms are crucial, he added.

A genuine or a pseudo economic and monetary union?

Two years ago, when the leaders approved the four president's report, titled "Toward a Genuine Economic and Monetary Union", I wrote that how genuine a union the euro area will be will depend on political will. For now, it seems that the ambition from the summer of 2012 is no longer there, but there seems to be a sober realisation of the fact that if the direction is toward a retreat from the rules, whose agreement consumed huge political energy in the past years, this will force the crisis back with new power and scale. Two events will prove whether the national leaders think soberly and responsibly for the others - how will the European Commission's recommendations be handled in mid-November and whether there will be a significant retreat from the 2012 road map for deepening of the integration of the euro area. Jose Manuel Barroso, the author of the more ambitious plan, praised the prime ministers and presidents of the euro area member states. According to him, key in their conclusions is that they will prepare the next steps for better economic governance of the eurozone.

It is very important to see what will these steps be. But even more important it will be to really find a way the member states to be forced to stick to their commitments. It all seems that in the future document this issue will be given special treatment. The third phase of the four presidents' report foresees the creation of something like a fund (fiscal capacity) offering financial incentives to countries that do deep reforms. In the same time, the Eurogroup chief started talking about the possibility to allow a deviation from the rules for countries whose structural reforms have been approved by the national parliaments. There are several ideas that are circulating about how this fund to be financed, but nothing is clear so far, except that the EU has a big chance to succeed if it does not allow exceptions for certain member states only because they believe they have a special position in the Union. It is not clear what is the need for a new report since the old one could have simply been updated. Let us hope that the reason behind this is not to postpone the solution of the problems further in time.

It is very important to see what will these steps be. But even more important it will be to really find a way the member states to be forced to stick to their commitments. It all seems that in the future document this issue will be given special treatment. The third phase of the four presidents' report foresees the creation of something like a fund (fiscal capacity) offering financial incentives to countries that do deep reforms. In the same time, the Eurogroup chief started talking about the possibility to allow a deviation from the rules for countries whose structural reforms have been approved by the national parliaments. There are several ideas that are circulating about how this fund to be financed, but nothing is clear so far, except that the EU has a big chance to succeed if it does not allow exceptions for certain member states only because they believe they have a special position in the Union. It is not clear what is the need for a new report since the old one could have simply been updated. Let us hope that the reason behind this is not to postpone the solution of the problems further in time.

Klaus Regling | © Council of the EU

Klaus Regling | © Council of the EU Mario Centeno | © Council of the EU

Mario Centeno | © Council of the EU Mario Centeno | © Council of the EU

Mario Centeno | © Council of the EU